How Japanese Firms Learned to Live With China

De-risking doesn't mean decoupling—at least not for most multinationals

Since the early 2010s, multinational corporations operating in China have faced mounting political risk. Notable episodes include anti-Japanese protests erupted in China after the 2012 Senkaku-Diaoyu territorial dispute, a standoff between Japan and China over control of contested islands in the East China Sea, posing a threat to Japanese business in the country. The U.S.-China trade war raised supply chain concerns, and COVID-19 lockdowns disrupted operations across the board. Governments have encouraged companies to reduce their reliance on the Chinese market. But have firms actually followed this advice, and if so, how?

Using Japan as a case study, a recent paper by Timothy Cichanowicz (University of Kansas), Jiakun Jack Zhang (University of Kansas), and Samantha A. Vortherms (University of California, Irvine) finds that 81 percent of Japanese multinationals, a group of companies long exposed to rhetoric and policy incentivizing independence from China, adopted at least one de-risking strategy between 2012 and 2022. However, outright exit from China remained rare. Instead, most firms pursued “diversification,” expanding operations elsewhere while staying put in China. The authors argue that national security concerns, rather than firm-level exposure to China, best explain which companies took the most decisive action.

The researchers introduce a typology to categorize firm responses to geopolitical risk. “Decoupling” means exiting China entirely. “Diversifying” means expanding investment outside China without reducing operations there. “Diverting” (or friend-shoring) involves both leaving China and reinvesting in allied countries. Firms that did none of these were classified as “business as usual.”

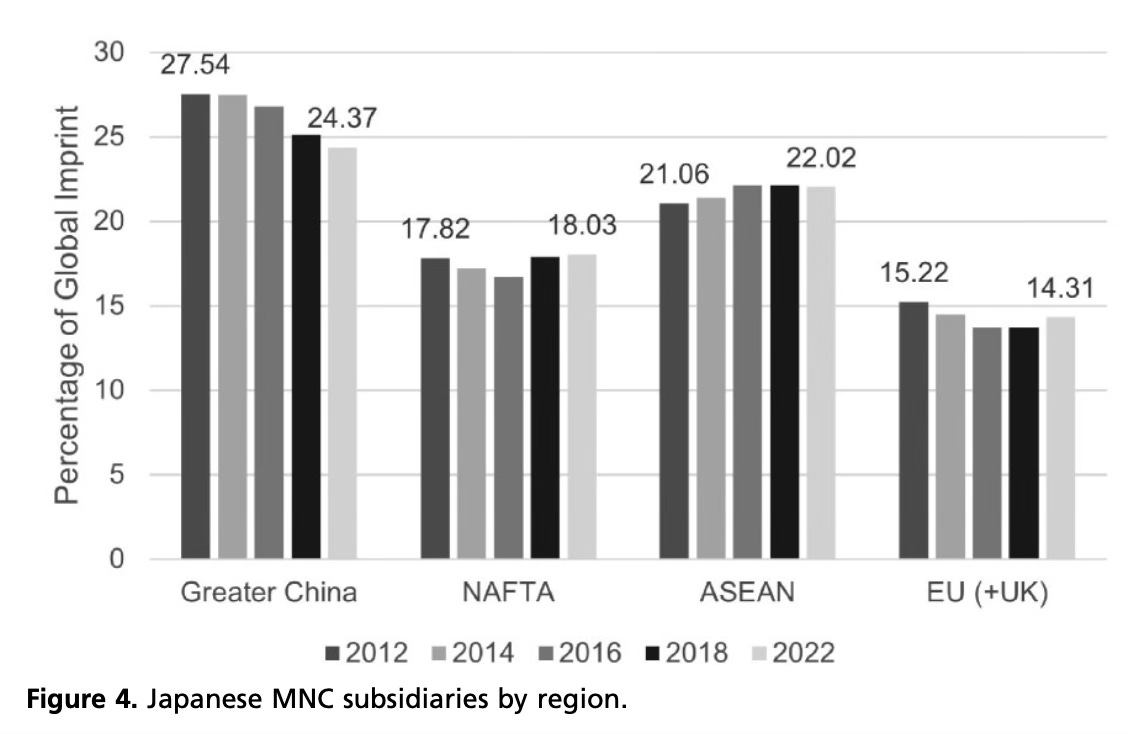

To determine what de-risking strategies companies employ, researchers tracked 100 Japanese firms with operations in China using registration data from China’s Ministry of Commerce and the Toyo Keizai Japanese Overseas Investment Yearbook. They observedsubsidiary openings and closures across multiple years spanning two periods of heightened political risk. First, the Senkaku-Diaoyu dispute (2012-2016) and, second, the trade war and pandemic era (2018-2022).

The results show that diversifying was the most common strategy, adopted by 43 percent of firms. Decoupling and friend-shoring each accounted for about 18-20 percent. Only 19 percent of firms did nothing. Among the firms that exited China and subsequently expanded elsewhere, nearly all reinvested in countries aligned with Japan—particularly the United States, Canada, Australia, and several ASEAN nations.

The paper’s most striking finding is that firms designated by the Japanese government as relevant to national security were significantly more likely to pursue all three de-risking strategies. This suggests that for firms in strategic sectors, the flag is clearly being followed, while for most Japanese companies, politics played a secondary role in investment decisions. The authors also did not find evidence that standard firm-level predictors like fixed asset investment in China, years of experience in the country, or dependence on Chinese operations predicted whether a firm chose to decouple, diversify, or friend-shore.

Some firms with particular vulnerabilities may be actively de-risking, but the findings suggest this is far from a general trend. In the case of Japan and China, most companies have hedged their bets by expanding operations elsewhere while maintaining their presence in the Chinese market, and China remains the largest destination for Japanese overseas investment. More broadly, the paper underscores how uneven and uncertain the relationship between political risk and corporate behavior really is, even after a decade of sustained pressure from governments hoping to reshape global supply chains.