Decoupling Has a Supply Problem

New research shows decoupling depends on who else can supply the goods

Over the past half century, the United States and China’s relationship has evolved extensively. Beginning with the normalization of relations under Nixon, U.S. policymakers pursued economic engagement with China, believing that integration into global markets would encourage cooperation, stability, and mutual prosperity. Over time, however, engagement produced deep economic entanglements that inflamed anti-Chinese sentiment. In recent years, rising geopolitical tensions have transformed these sentiments into a desire for economic decoupling. Evidence suggests growing distance between the two countries, if not complete independence. China’s share of total U.S. imports fell from 21.6 percent in 2017 to 13.3 percent by 2023.1 China’s share of U.S. exports and investment also declined during the same timeframe.2

Against this backdrop, Ayse Eldes, Jieun Lee, and Iain Osgood’s paper, Allied Import Options Available? Finding Friendly Trade Partners Amidst Decoupling from China, investigates the conditions under which firms reduce reliance on Chinese markets. The authors argue that the feasibility of decoupling depends heavily on market conditions—specifically, the availability of viable alternative suppliers in geopolitically aligned countries. They find that US imports from China in the post-Trade War era decreased among products with alternative suppliers in allied nations, but not those where alternatives were primarily located in hostile states. For products without friendly suppliers, firms were more likely to request exemptions from tariffs.

The authors suggest decoupling presents several major challenges. Firms face substantial costs when switching suppliers or relocating production. More fundamentally, viable alternative suppliers may not exist. For some products, China accounts for the overwhelming majority of supply. Even if there are other producers, political considerations complicate relocation decisions, as moving production from China to another non-allied state may replicate similar geopolitical risks rather than reduce them. These challenges, the authors argue, mean firms will only remove China from their supply chains if there are suppliers who can provide equivalent products in significantly less risky countries.

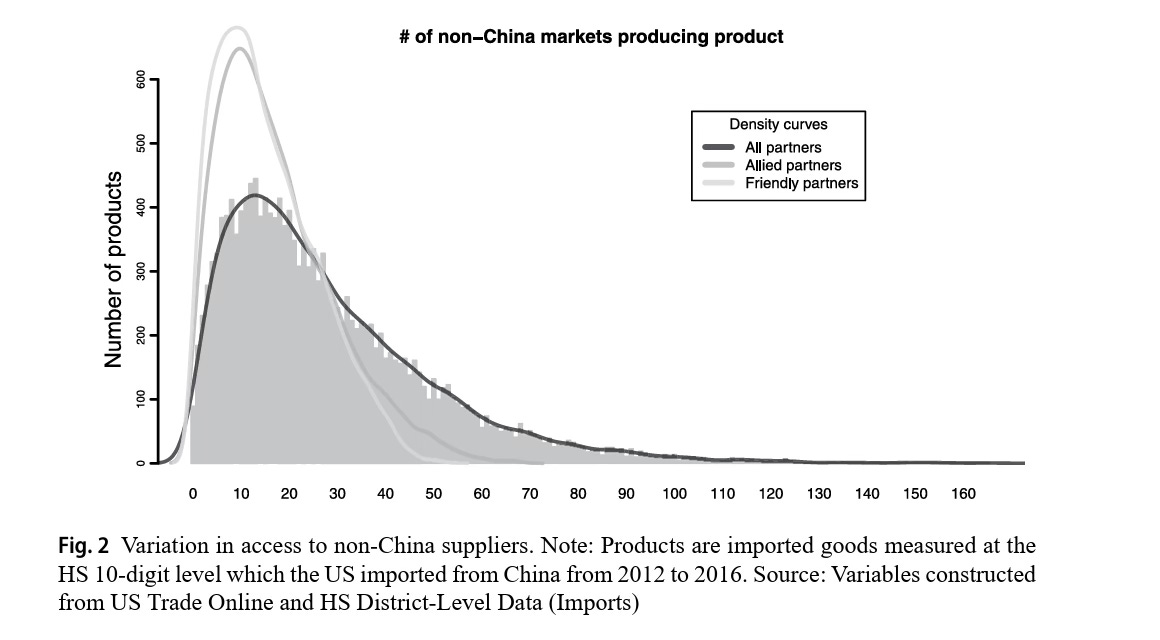

To test their theory, the authors analyze product-level U.S. import data during the initial years of the trade war (2018–2020) and extend their analysis through the early years of the Biden administration (2021–2023). Their findings show products with numerous alternative markets experienced import declines of roughly 29–34 percent on average following the trade war’s onset, with reductions exceeding 40 percent in the 2021–2023 period. In contrast, imports declined far less for products with limited alternative suppliers.

Crucially, these effects are driven almost entirely by the availability of allied or friendly alternative markets. When the number of allied suppliers doubles, imports from China fall by roughly 11–14 percent more than products with fewer allied suppliers in the early trade war period, and 15–20 percent more in the Biden era. By contrast, the presence of economically viable but non-allied suppliers has no statistically significant effect on import reductions. Firms appear reluctant to substitute China with another potential strategic competitor. Overall, the evidence demonstrates that firms are more likely to exit China when they have access to diverse and politically secure supply options. Where such alternatives are unavailable, firms remain tied to Chinese production networks despite policy pressure.

To complement their trade analysis, the authors examine an alternative firms have to shifting supply chains: requests for products to be exempt from tariffs. The findings mirror the trade results. Products with greater availability of alternative suppliers—especially in allied or friendly markets—received significantly fewer exclusion requests. Conversely, when alternative markets were limited, firms sought regulatory relief in order to maintain existing supply relationships. The magnitude of these effects is substantial, but, as with import adjustments, the presence of non-allied suppliers has little effect. Firms are more likely to resist trade restrictions when allied alternatives are unavailable.

The paper makes several important contributions to the broader literature on international political economy. First, it develops a political theory of decoupling that emphasizes both motive and capacity: rising policy and geopolitical risk creates incentives to exit, but firms can only do so when viable alternatives exist in geopolitically aligned markets. Second, the availability of alternative suppliers reduces firm opposition to trade restrictions, contributing to research showing limited political mobilization among firms during the U.S.–China trade war. More broadly, the findings inform ongoing debates about the feasibility of large-scale economic decoupling. The research suggests that meaningful supply chain restructuring requires not only policy incentives, but also the development of reliable alternative production relationships in politically secure markets.

Bureau of Economic Analysis “U.S. Direct Investment Abroad, U.S. Direct Investment Position Abroad on a Historical-Cost Basis” available at https://www.bea.gov/itable/direct-investment-multinational-enterprises

Bureau of Economic Analysis “U.S. Direct Investment Abroad, U.S. Direct Investment Position Abroad on a Historical-Cost Basis” available at https://www.bea.gov/itable/direct-investment-multinational-enterprises

|

|